Powered by .id (informed decisions) for City of Sydney

.id community is an evidence base for over 250 local government areas in Australia and New Zealand, helping you make informed decisions.

LEARN MORE ABOUT .idThe City of Sydney was the location of the first European settlement in Australia. The City of Sydney has developed from colonial settlement to village to town to major world city.

The extent of redevelopment proposed over the next ten years will see the City return to population levels unseen since the 1920s. This is expected to occur through massive numbers of new dwellings being constructed, although the average numbers of persons occupying each dwelling will be far lower than in earlier decades.

The City has been affected by the impact of COVID-19, especially in the those areas of the City with large numbers of tertiary students, particularly overseas students. In total, owing to the pandemic, Sydney has seen a net loss of approximately 45,000 persons to overseas migration. This is assumed to be a short-term effect caused by NSW’s lock-down and the closure of international borders, and that the migration patterns experienced prior to the pandemic will return over the next year now that those restrictions have been removed. In particular it is expected that there will be a return to the large levels of overseas in-migration experienced prior to the pandemic. This will also see a return to high levels of housing demand, fuelling in particular the development of higher density residential housing in the established areas of the City.

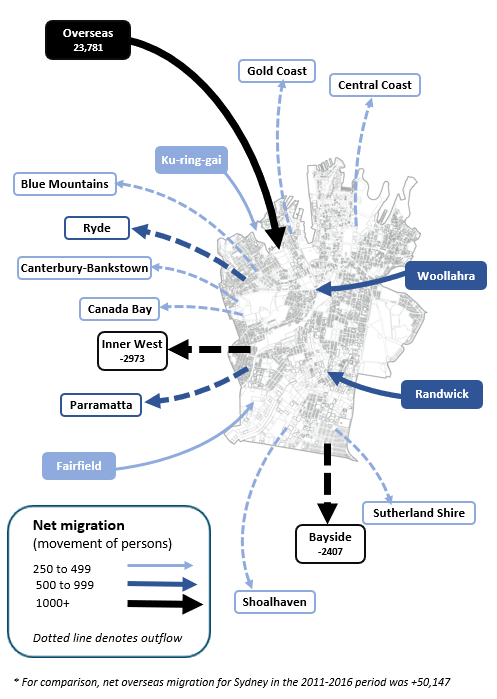

The City also attracts large numbers of migrants from regional New South Wales and interstate, the bulk of these being young people studying or moving to Sydney for lifestyle and/or employment reasons. The City of Sydney is the most familiar part of the metropolitan area for those not from the metropolitan area and is therefore attractive to migrants not only from regional New South Wales but also from interstate. The eastern suburbs of Sydney also provide a net flow of migrants to the City of Sydney. This may be the result of greater affordability in the southern suburbs of the City of Sydney.

Note: The migration flows depicted above are historical and do not represent future or forecast migration flows or subsequent council boundary changes. The arrows represent migration flows to the area as a whole and do not indicate an origin or destination for any specific localities within the area. Overseas flow shows overseas arrivals based on answers to the census question "where did the person usually live 5-years ago" and .id estimates of international out-migration.

*Please note, the 2021 Census was undertaken during the COVID-19 pandemic, at a time where border restrictions had largely halted overseas in-migration for the 15 months prior. 2016-2021 net overseas migration levels reflect this and therefore should not necessarily be considered indicative of longer-term trends.

Many other areas (eg King Street small area and Chinatown & CBD South small area) are also expected to have significant levels of development.

The built form that is expected with these developments is likely to shape the population. The majority of new dwellings that are expected to be built over the forecast period are apartments, many of which are relatively small in nature (one and two bedroom). The apartment market has been dominated by young singles, couples and students.

There are a number of key markets that are being targeted by developers. 1-bedroom apartments are mainly aimed at the student market and owned by investors. A number of developments have between 50% to 75% students (majority overseas), most of which is owned by investors. These sorts of developments are more likely to have younger university-aged populations.

2 and 3 bedroom apartments are aimed at young urban professionals with some investor elements, a part of which is emerging empty nesters and empty nesters providing accommodation for their children while at university. These developments are more focussed on comparatively high double-income households. Most apartment developments have penthouse components (1%), where dwellings can be well in excess of $1 million. This market is not easily identified, although corporate apartments may form a significant share of this market.

As a result of these different tenure relations, it is common to have a wide variety of vacancy rates across the City of Sydney. Areas with a large supply of dwellings are more likely to have a high vacancy rate due to the considerable stock being introduced into the market. This is heightened in areas, where the majority of residents are renters and further exaggerated where there are many corporate apartments, temporary stay accommodation and non-permanent residences.

There is significant potential volatility in the housing market of the City of Sydney over the next fifteen years due its dependence on a number of factors. These include:

DISCLAIMER: While all due care has been taken to ensure that the content of this website is accurate and current, there may be errors or omissions in it and no legal responsibility is accepted for the information and opinions in this website.

Please view our Privacy Policy, Terms of use and Legal notices.

ABS Data and the copyright in the ABS Data remains the property of the Australian Bureau of Statistics. The copyright in the way .id has modified, transformed or reconfigured the ABS Data as published on this website remains the property of .id. ABS Data can be accessed from the Australian Bureau of Statistics at www.abs.gov.au. ABS data can be used under license - terms published on ABS website. intermediary.management@abs.gov.au if you have any queries or wish to distribute any ABS data.